Fixed costs planning: why fixed costs shape your month

Fixed costs often decide your real spending room before daily choices do. Learn how FlowyZ makes recurring payments visible in your monthly cashflow.

Fixed costs are easy to overlook because they feel familiar. Rent, mortgage, energy, insurance, phone, internet, subscriptions, savings transfers and software payments often return every month. Because fixed costs are known, they can seem simple. Still, fixed costs are often the reason a month feels different from the balance in your banking app.

Your bank shows what is available today. Fixed costs show what still has to happen. That difference matters. If you only react to fixed costs after they have been debited, you are looking backward. Cashflow planning is about looking ahead. FlowyZ is built to place recurring payments in your month so you can see earlier how much room is really left.

This article explains why fixed costs are the backbone of a monthly cashflow plan, how to organize them in a practical way and why FlowyZ can be convenient if you want less dependence on memory, bank alerts or a spreadsheet that is always slightly out of date.

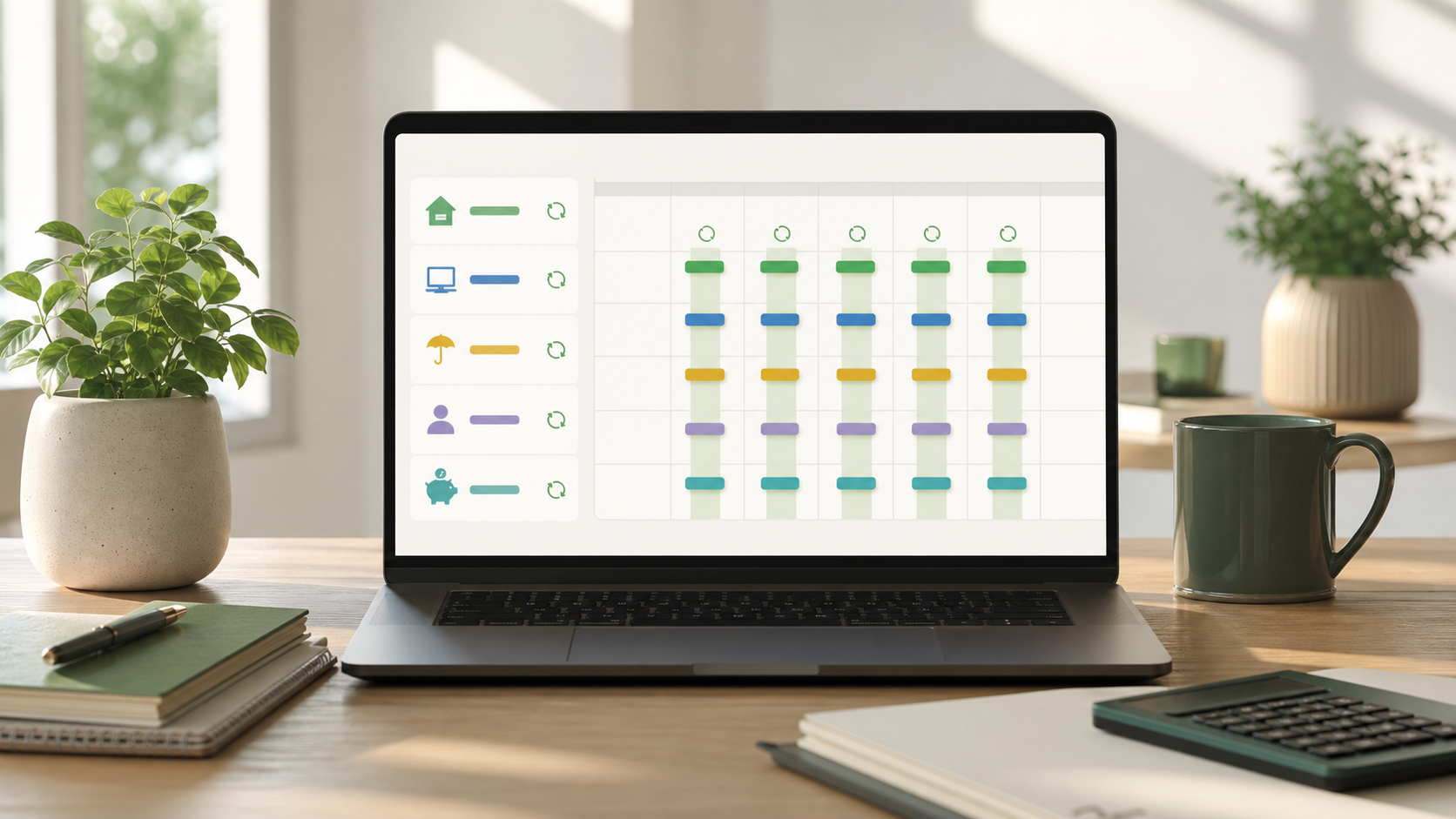

Fixed costs are about timing, not only amount

Many people think about fixed costs as amounts. What is the rent? What is the energy bill? What do insurance and phone contracts cost? Those numbers matter, but they are only half of the picture. The timing of fixed costs decides how the month feels.

A month with 1800 euros in fixed costs can feel manageable when income arrives first and payments are spread out. The same fixed costs can feel heavy when almost everything leaves in the first week. In that case the issue is not only how much you pay, but when you pay it.

FlowyZ places fixed costs on a timeline. You see the sequence, not only the total. Does salary arrive before rent? Does an annual insurance payment hit in the same week as subscriptions? Is the savings transfer too early in the month? When those questions are visible, fixed costs planning becomes a concrete view instead of a rough guess.

That view helps with ordinary choices. You do not have to wait until the account feels tight. You can see earlier whether the month still has space for groceries, transport, small purchases and unexpected costs after all fixed costs are counted.

Why fixed costs are often underestimated

Fixed costs are underestimated because they are familiar. You roughly know what is coming, so it feels under control. In practice, most people have more recurring payments than they remember.

Besides the large items, there are small fixed costs. Streaming, cloud storage, software, sport, donations, bank fees, insurance add-ons, maintenance, school costs and automatic savings rules can all repeat. Alone they look small. Together they can take a serious part of your free space.

The problem is that fixed costs arrive across the month. One payment is on day one, another on day twelve, another near the end. You notice the individual debits, but you may not see the total pattern.

Cashflow planning makes that pattern visible. In FlowyZ, fixed costs can be entered as recurring items. Each month then starts with the known obligations already in view. You do not have to rebuild the list from memory and you do not have to rely on an old spreadsheet that slowly becomes less accurate.

A good fixed costs list is not a strict budget. It is a map of commitments. When that map is correct, the rest of the month becomes easier to steer.

Fixed costs and variable spending need different treatment

Fixed costs are predictable. Variable spending moves with daily life. Groceries, fuel, going out, clothing, gifts and small repairs are less exact. But variable spending only makes sense after fixed costs have been included.

Imagine there is 900 euros in the account. Without planning, that can look comfortable. If 650 euros in fixed costs are still coming, the free space is much smaller. If the fixed costs have already been paid, the same balance means something very different.

That is why fixed costs should be the first layer of the month. After that, variable spending can be judged more honestly. The useful question is not only how much money is visible today. The useful question is what remains after known payments and fixed costs are included.

FlowyZ supports that by showing planned income, fixed costs and one-off items together. You can see an expected closing balance and adjust before stress builds. That does not make recurring payments pleasant, but it does make them clearer.

For households, this helps with normal decisions. For freelancers and small teams, it is just as useful because business recurring payments continue even when income changes from month to month.

Recurring payments create calm when they are accurate

recurring payments only create calm when the list is complete and current. A plan with missing recurring payments can be misleading. That is why recurring payments should be reviewed from time to time.

Start with the largest recurring payments. Rent, mortgage, energy, insurance, phone, internet and major subscriptions are usually easy to find. Then add smaller items. Also look for annual or quarterly recurring payments that do not appear every month, such as taxes, maintenance, licenses, memberships or insurance renewals.

In FlowyZ, these items can be planned as recurring payments. That means recurring payments return automatically in the monthly view. If an amount changes, you update the rule. If a subscription stops, you remove it. The overview keeps moving with reality.

The goal is not to predict every euro perfectly. The goal is to stop carrying recurring payments in your head. Once recurring payments are set up, you mostly have to review exceptions. That saves attention.

A small habit helps: check recurring payments once a month. This does not need to become a long administration session. Ten minutes can be enough to spot changed rates, cancelled subscriptions or payments that no longer belong in the plan.

recurring payments make free space more honest

Free space is not the same as balance. Free space is what remains after recurring payments, planned spending and known obligations have been taken into account. That distinction prevents wrong conclusions.

A high balance before recurring payments are debited can feel too optimistic. A lower balance after recurring payments are paid can actually be calmer than it looks, because the biggest obligations are already handled. Without planning, that difference is hard to see.

FlowyZ lets recurring payments count in the expected movement of the month. You can see whether money is truly available or only temporarily sitting in the account. This is especially important around salary, rent, taxes, insurance and automatic savings.

This way of looking makes decisions more concrete. Can you make a purchase? Should a savings transfer move later? Is there room for a repair? Should you chase an invoice sooner? The answer often depends less on today’s balance and more on the recurring payments still ahead.

When recurring payments are planned first, there is less internal debate. The commitments are visible. Then you can decide what to do with the remaining money more deliberately.

Annual recurring payments need their own place

Not all recurring payments are monthly. Some recurring payments arrive quarterly or yearly. These items create surprises because they do not fit the normal monthly feeling.

Think about insurance, local taxes, software licenses, maintenance, membership fees, school costs or yearly service contracts. If you forget these recurring payments, the month can seem fine until the large payment appears. It feels like a problem, even though the payment was predictable.

A practical approach is to place annual recurring payments in the month when they occur. An even calmer approach is to reserve for them gradually. Not everyone wants separate saving pots, but everyone benefits from seeing the peaks before they arrive.

FlowyZ helps by placing those peaks in the plan. You can see that a certain month will be heavier and make choices earlier. Maybe you delay a purchase, hold more buffer, move a savings transfer or prepare for a lower closing balance.

Without an overview, annual recurring payments appear as surprises. With cashflow planning, they become normal parts of the year.

recurring payments across multiple accounts

recurring payments become more complex when you use more than one account. A personal account, joint account, savings account and business account can all matter. Then the question is not only which recurring payments are coming, but also which account they leave from.

A joint account may have enough for rent and energy while the personal account is tight. A business account may contain money that is really meant for taxes, software or suppliers. Savings can provide buffer, but that does not automatically mean free spending room.

Planning recurring payments per account helps you see where pressure appears. The total may be fine, but the money may be in the wrong place. There may be enough balance overall, but not on the account where the debit happens.

FlowyZ is useful because accounts, categories and planned payments can be viewed together. recurring payments planning becomes practical, not just theoretical. It shows whether the month can actually run through the right accounts.

That prevents simple but irritating problems: an automatic debit arriving too early, a joint account that needs a manual top-up or a savings transfer that would be better later in the month.

How to start with FlowyZ

Start simple. Add your most important recurring payments to FlowyZ. Add expected income. Then look at the expected closing balance. Does it match your feeling? If it does not, that is useful information.

After that, refine the plan. Add smaller recurring payments, group them into categories and create recurring rules. Later you can process real transactions or import CSV files if you want to compare planning with reality. It does not need to be perfect on day one.

The value comes from having recurring payments in one reliable place. Not scattered across bank notifications, not carried in your head and not hidden in a spreadsheet you only open when stress has already started. In FlowyZ, recurring payments planning becomes part of the month.

Related FlowyZ guides

For the broader overview, read cashflow planning with FlowyZ. Related guides:

For general consumer finance information, you can also read resources from the Consumer Financial Protection Bureau. If you want to look ahead at your own month, start with the FlowyZ website.

A simple recurring payments routine

A useful routine can stay small. Choose a moment at the start of the month. Check which recurring payments are planned. Look at whether income and debits fall in a logical order. Then check halfway through the month for anything unusual.

This routine creates calm because recurring payments stop appearing as disconnected surprises. You see what is still coming, what has already been paid and what is likely to remain. That makes it easier to adjust in time.

recurring payments do not disappear because you plan them. But recurring payments become less dominant when you see them earlier. That is the practical value of cashflow planning: known payments turn from background noise into structure.

FlowyZ tries to make that structure usable. Not with complicated financial theory, but with a clear monthly view. When recurring payments are correct, the rest of your money decisions become more honest, calmer and easier to understand.